Module 4: Enterprise Value/Comparables

Recruiting | Behaviorals | Accounting | Enterprise Value / Comparables | DCF | M&A | LBO| Market questions | Brain teasers

Valuation Fundamentals: Mastering Market-Based Techniques

This module builds your fluency in how companies are valued through market-based approaches. You’ll learn the core differences between equity value and enterprise value, how to calculate and interpret key valuation multiples like EV/EBITDA and P/E, and how to run a comparables analysis. Lessons also walk through precedent transactions, the treasury stock method, and sum-of-the-parts analysis. Whether you’re preparing for interviews or building pitchbooks, this is where you learn to speak the language of valuation with clarity and precision.

Lesson 1

Enterprise Value Formula and Equity Value

Enterprise value and equity value are two core valuation concepts in finance, and understanding how to calculate and interpret them is fundamental for investment banking. This lesson covers the conceptual difference, the formulas, and why elements like preferred equity and net debt matter.

In this Lesson:

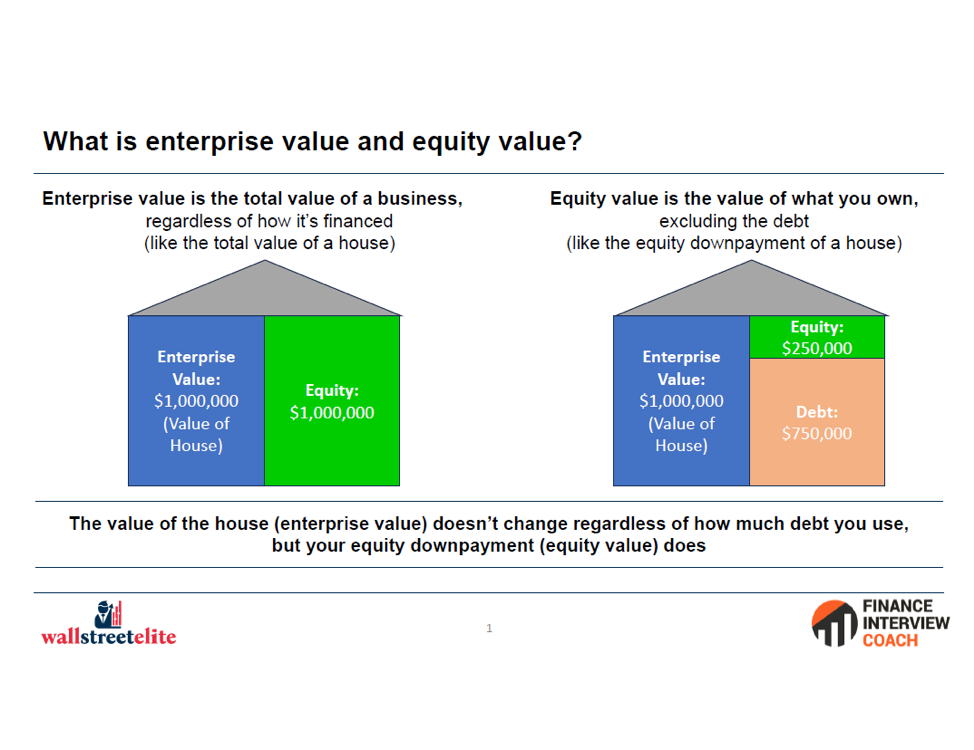

- Enterprise Value: Total value of a business regardless of how it’s financed.

- Equity Value: Portion of the business owned by shareholders after subtracting debt.

- House Analogy: A $1M house has the same enterprise value whether financed with debt or equity—only equity value changes.

- Simple Formula: EV = Equity Value + Net Debt, where Net Debt = Debt – Cash.

- Equity Value Formula: Equity Value = Share Price × Shares Outstanding.

- Full EV Formula: EV = Equity Value + Debt – Cash + Preferred Equity + Minority Interest.

- Preferred Equity: Hybrid of debt and equity—gets paid before common equity and is included in EV.

- Why Include It: Preferred equity reflects additional claims on cash flow and affects total acquisition cost.

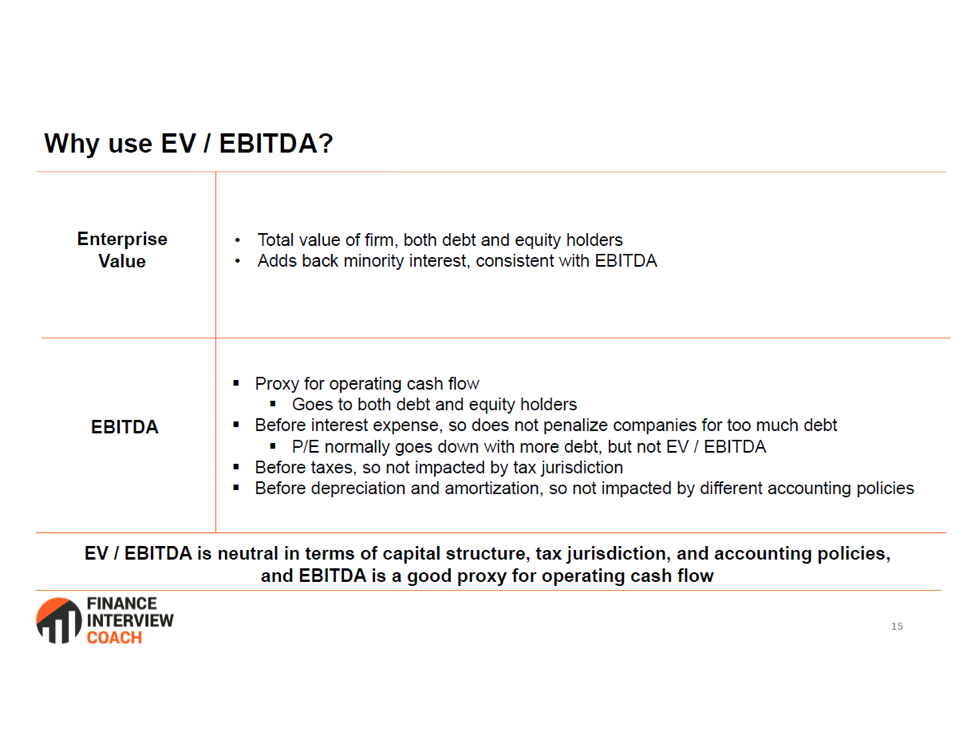

- IB Relevance: EV is used in capital-structure-neutral multiples (e.g., EV/EBITDA), while Equity Value drives per-share metrics.

Lesson 2

EV / EBITDA vs. P / E and other key multiples

Valuation multiples are a core part of investment banking, and understanding the differences between EV/EBITDA and P/E is essential for comparing companies correctly. This lesson explains how to use each multiple, what they measure, and why adjustments like non-controlling interest are crucial for accuracy.

In this Lesson:

- Core Definitions: Explain EV/EBITDA (capital-neutral) vs. P/E (equity-focused) and what each measures.

- Usage Scenarios: When to use EV/EBITDA vs. P/E based on company leverage and earnings consistency.

- Capital Structure Impact: EV multiples ignore debt/equity mix; P/E reflects it.

- Limitations: EV/EBITDA ignores capex; P/E distorted by taxes or non-cash items.

- Industry Relevance: Which sectors favor which multiples (e.g., EV/Revenue for SaaS).

- Valuation Link: How multiples drive implied share price or enterprise value.

Lesson 3

Key drivers of multiples - why some companies are more expensive than others

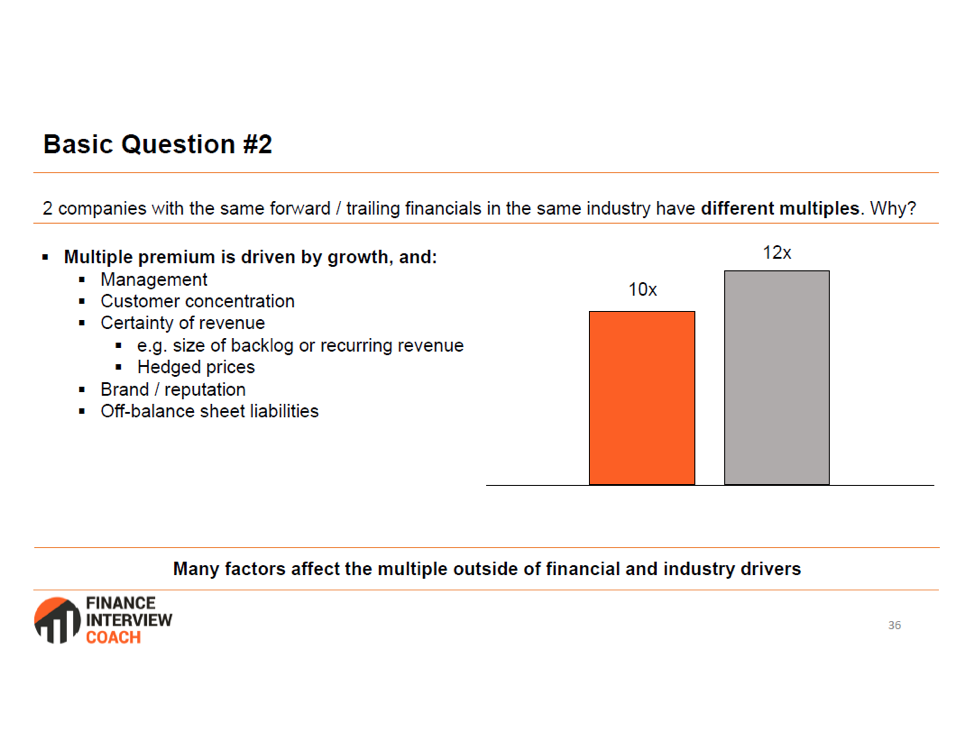

Not all companies are valued equally. Differences in growth, profitability, and risk lead to wide variations in valuation multiples. This lesson explores the key drivers that make some companies more “expensive” than others, including margin strength, return on capital, competitive advantages, and market leadership.In this Lesson:

- Growth: Faster-growing firms trade at higher multiples due to future cash flow potential.

- Margins: Higher EBITDA or net income margins boost valuation.

- Return on Capital: Strong ROIC or ROE signals efficient capital use and commands a premium.

- Risk Profile: Stable, low-risk businesses get higher multiples than cyclical or volatile ones.

- Competitive Moat: Brand strength, IP, or market dominance drives valuation premiums.

- Scale and Market Position: Larger firms or market leaders often trade at higher multiples.

Lesson 4

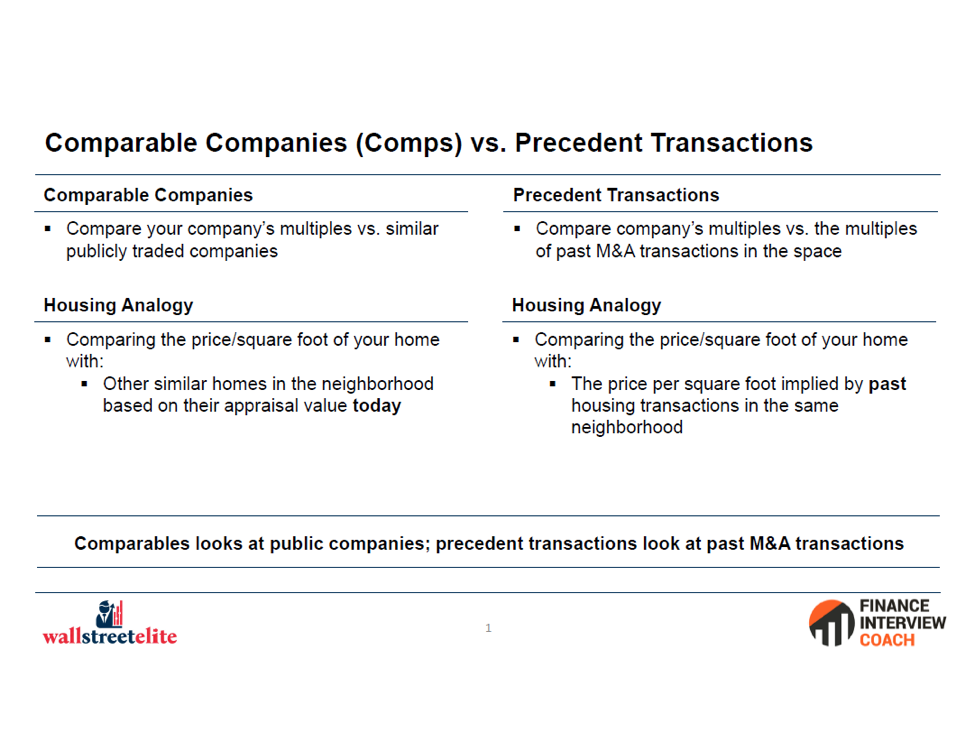

Comparables Analysis

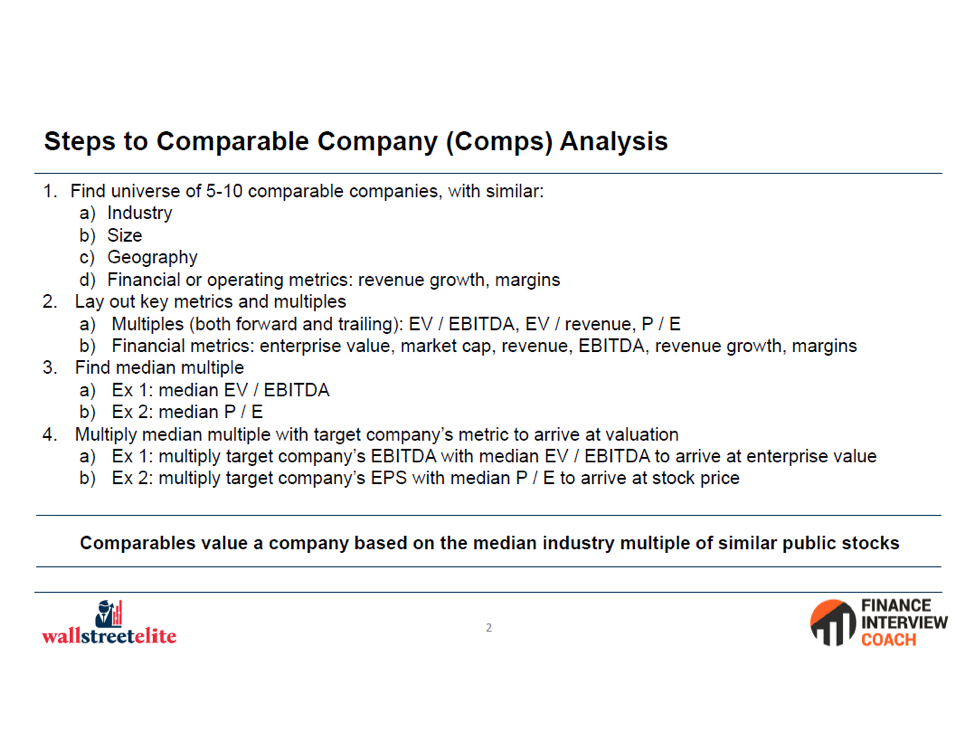

Comparable company analysis is one of the most commonly used valuation methods in investment banking. This lesson walks through how to identify comps, calculate valuation multiples, and understand when and why this method is used.

In this Lesson:

- Core Concept: Value a company based on how similar public firms trade.

- Selection Criteria: Choose comps based on industry, size, growth, and margins.

- Key Multiples: Use EV/EBITDA, P/E, EV/Revenue depending on sector.

- Normalization: Adjust for non-recurring items, leases, or accounting differences.

- Valuation Range: Derive high, low, and median multiples to value target.

- Use Cases: Common in pitchbooks, fairness opinions, and benchmarking.

Lesson 5

Precedent Transactions

Precedent transactions analysis is a core valuation method that looks at prices paid in real M&A deals to estimate what a company is worth. This lesson explains how to find relevant deals, calculate valuation multiples, and understand when this method provides higher or lower valuations than comparables.

In this Lesson:

Core Concept: Value a company based on prices paid in past M&A deals.

Relevance: Reflects real buyer behavior and control premiums.

Selection Criteria: Match by industry, size, timing, and deal type.

Key Multiples: Focus on EV/EBITDA, EV/Revenue at time of acquisition.

Premiums Paid: Capture takeover premium over unaffected share price.

Lesson 6

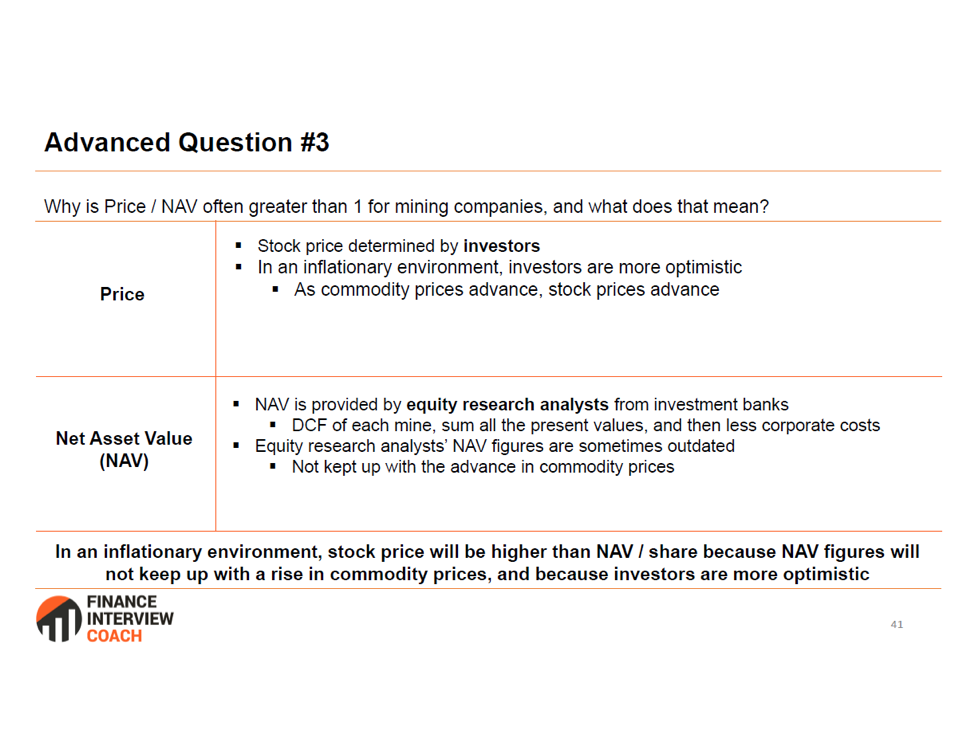

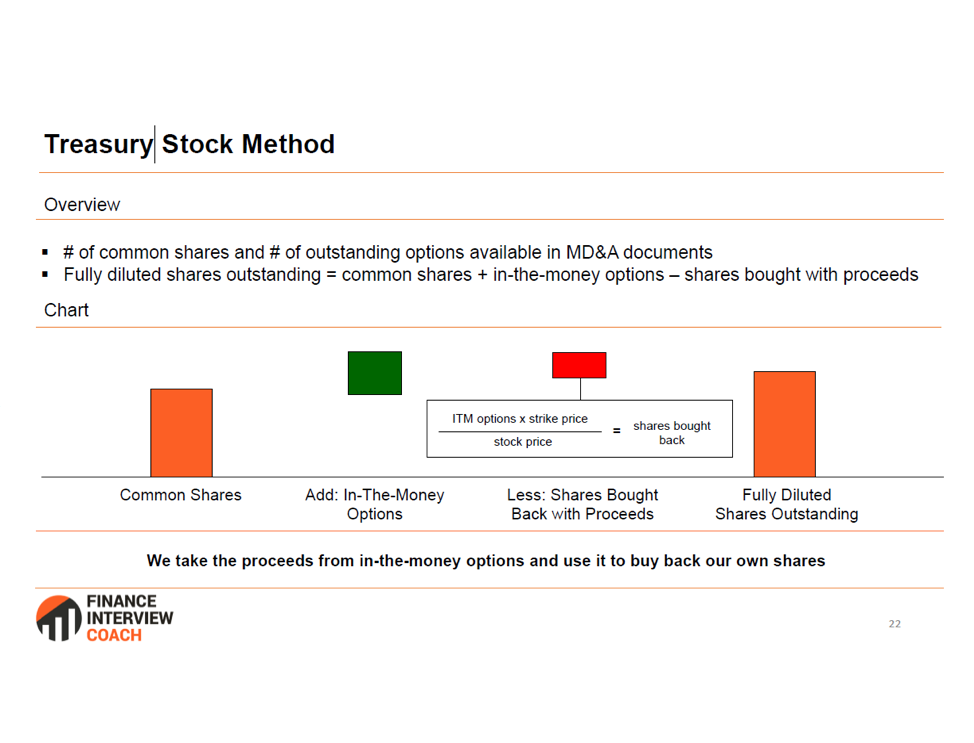

Treasury stock method (Coming Aug 8)

The Treasury Stock Method is a key concept for modeling dilution from employee stock options and warrants. This lesson explains how TSM estimates net new shares added to the count, by assuming options are exercised and proceeds are used to buy back shares, impacting diluted EPS and equity value per share.

In this lesson:

- Core Concept: Calculates dilution from in-the-money options and warrants

- How It Works: Assumes proceeds from exercised options are used to repurchase shares.

- Diluted Shares: Net new shares = options exercised minus shares repurchased.

- Impact on Valuation: Increases fully diluted share count, lowering per-share metrics.

- Key Inputs: Stock price, strike price, and number of options.

- Common Use: Used in calculating diluted EPS and equity value per share.

Lesson 7

Different valuation methods and how to rank them (Coming Aug 10)

Valuation methods differ in approach, reliability, and use case, some reflect market sentiment, while others estimate intrinsic value. This lesson compares key methods like public comps, precedent transactions, DCF, LBO, and SOTP, and explains how to rank or prioritize them based on the company, data availability, and transaction context.

In this lesson:

- Public Comps: Market-based, widely used; good for benchmarking.

- Precedent Transactions: Reflects control premiums; often yields higher values.

- DCF (Discounted Cash Flow): Intrinsic value; sensitive to assumptions.

- LBO Analysis: Floor valuation based on sponsor returns and leverage.

- SOTP (Sum of the Parts): Best for diversified businesses; values each unit separately.

- Ranking: DCF and LBO = intrinsic; Comps and Precedents = market-based; rank based on context, data quality, and deal purpose.

Lesson 8

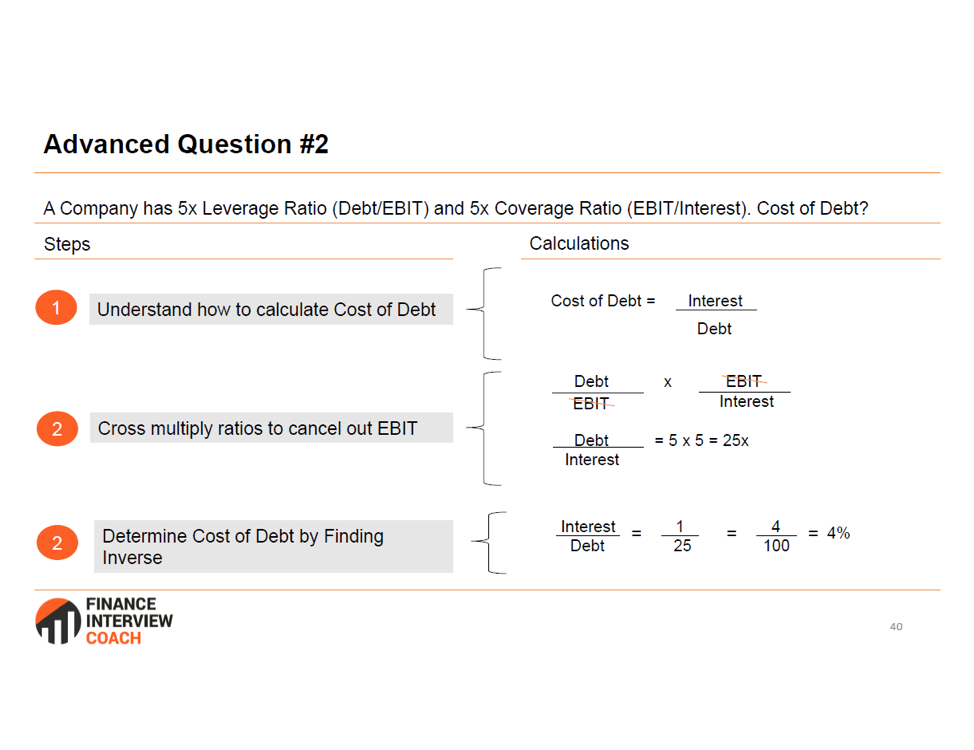

Key debt metrics (Coming Aug 24)

Understanding key debt metrics is essential for analyzing a company’s creditworthiness and capital structure. This lesson covers core ratios like Total Debt/EBITDA and Interest Coverage, along with fixed charge metrics and credit ratings, tools bankers use to assess leverage, repayment capacity, and overall financial risk.

In this lesson:

- Total Debt / EBITDA: Measures leverage and ability to repay debt with earnings.

- Net Debt / EBITDA: Adjusts for cash; shows true leverage position.

- EBITDA / Interest (Interest Coverage): Assesses ability to meet interest payments.

- Debt / Equity: Compares financing mix between debt and equity.

- Fixed Charge Coverage: Includes lease and interest obligations.

- Credit Ratings: Reflect perceived default risk by agencies like S&P or Moody’s.

Lesson 9

Sum of Parts Analysis (Coming Aug 28)

Sum of the Parts analysis is used to value complex or diversified companies by assessing each business unit individually. This lesson explains how to apply separate valuation methods to segments, adjust for net debt and corporate items, and when it’s is most useful, especially in M&A and fairness opinions.

In this lesson:

- Use Cases: Common in fairness opinions and M&A pitch materials

- Core Concept: Value each business segment separately, then sum total.

- Use Case: Ideal for diversified or conglomerate companies.

- Segment Valuation: Apply different multiples or DCFs to each unit.

- Adjustments: Subtract net debt and add corporate assets or liabilities.

- Challenges: Requires detailed segment data and peer comps.

Josh is a leader in interview preparation and career development. Josh was instrumental in helping me land a job at a leading global investment bank in NYC. Josh continues to be a source of guidance and mentorship as I progress through my career. I highly recommend working with Josh to secure your next job in the financial industry.

DD

Start your IB prep today.

Don’t wait to get ahead—start your IB prep today.