Module 3: Accounting

Recruiting | Behaviorals | Accounting | Enterprise Value / Comparables | DCF | M&A | LBO| Market questions | Brain teasers

The Foundation of Every Deal

Mastering accounting is essential for acing technical interviews and building accurate financial models. This module breaks down the three core financial statements—income statement, balance sheet, and cash flow statement—and shows you how they link together in real IB scenarios. You’ll learn how to analyze working capital, model depreciation, and interpret earnings quality with confidence. Whether you’re preparing for interviews or building your first LBO, this is where your technical foundation gets built.

Lesson 1

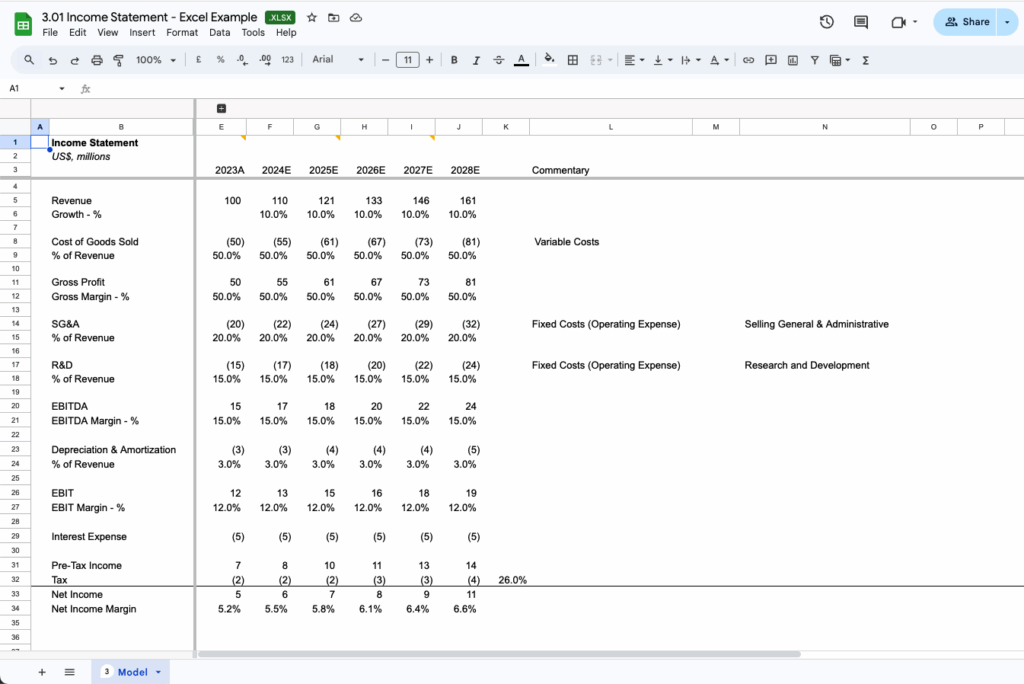

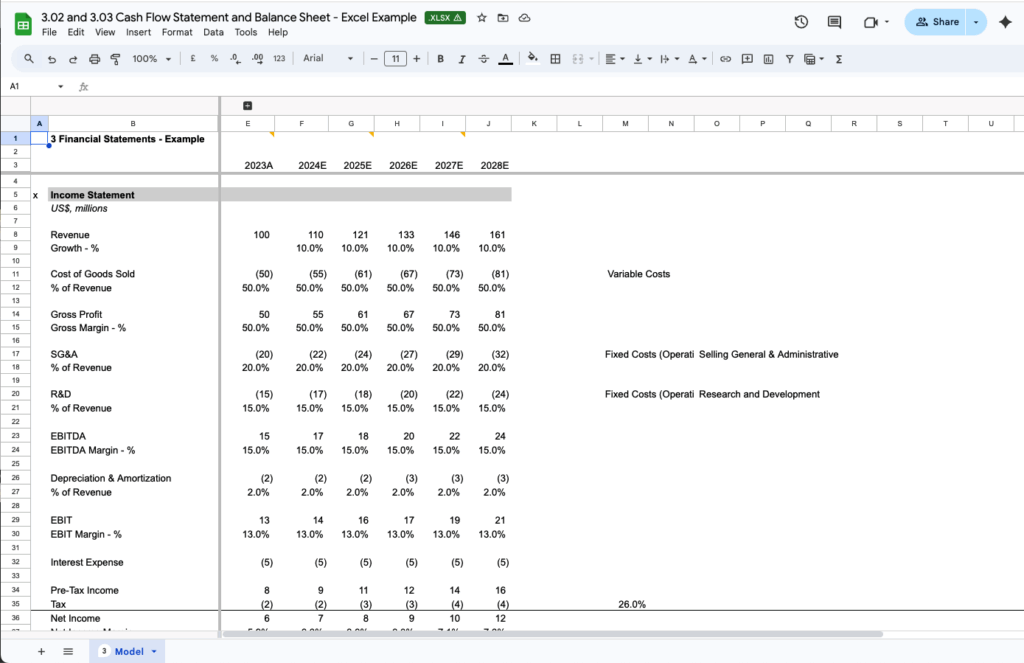

Income Statement

Whether you’re analyzing a company’s performance or preparing for technical interviews, mastering the income statement is a foundational skill in investment banking. This lesson walks through how it works, what it tells you, and how it connects to broader financial analysis.

In this Lesson:

- Core Purpose: Shows a company’s profitability over a given period.

- Top Line: Begins with revenue (sales) — often broken out by segment or product.

- Cost Structure: Subtracts COGS, OpEx (SG&A, R&D) and D&A to calculate operating income (EBIT).

- Non-Operating Items: Includes interest, taxes, and other income/expenses.

- Bottom Line: Ends with net income — key for EPS and equity value.

- IB Relevance: Used for comps, projecting margins, and building LBO and DCF models.

Lesson 2

Cash Flow Statement

While the income statement shows profitability, the cash flow statement reveals what really matters—how much cash a company generates and where it goes. This lesson breaks down how to read and analyze the cash flow statement, and why it’s essential for investment banking and valuation work.

In this Lesson:

- Three Sections: Operating, Investing, and Financing activities.

- Start with Net Income: Reconciles to cash via non-cash add-backs like D&A and changes in working capital.

- Investing Activities: Tracks capex, acquisitions, divestitures, and investments.

- Financing Activities: Reflects changes in debt, equity issuance/buybacks, and dividends.

- Final Output: Ending cash balance reconciles with the balance sheet.

- IB Relevance: Key to understanding FCF and how a company funds growth.

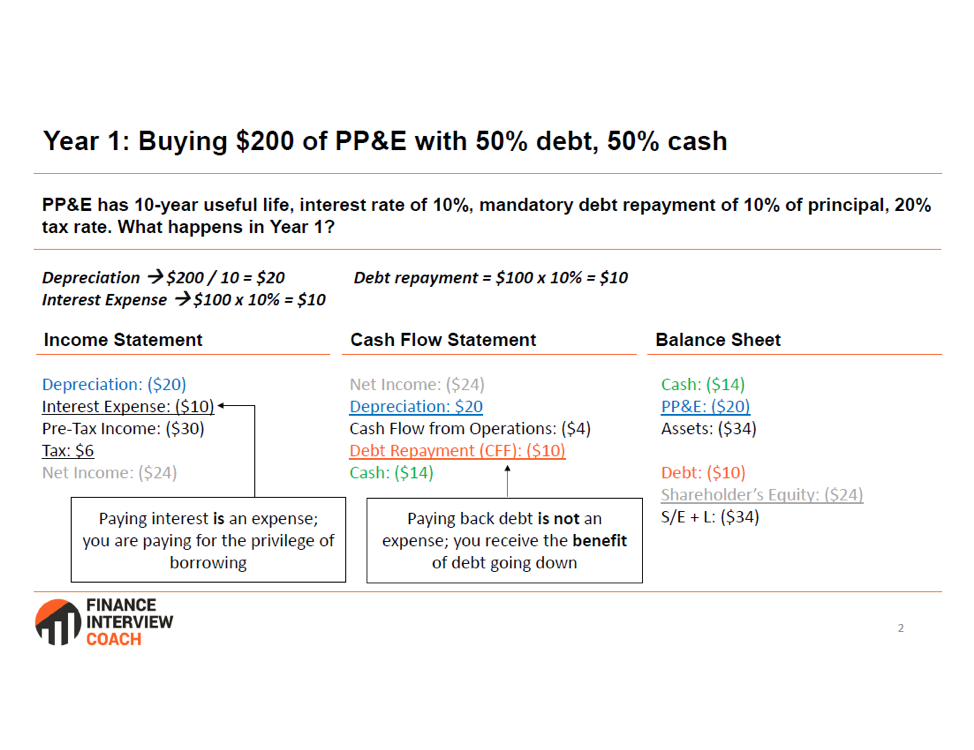

Property Plant and Equipment (PP&E)

We’ve helped over 1000 students and career switchers break into bulge brackets, elite boutiques, and top middle market firms with proven frameworks, real interview questions, and technical training that replicates the job.

Lesson 3

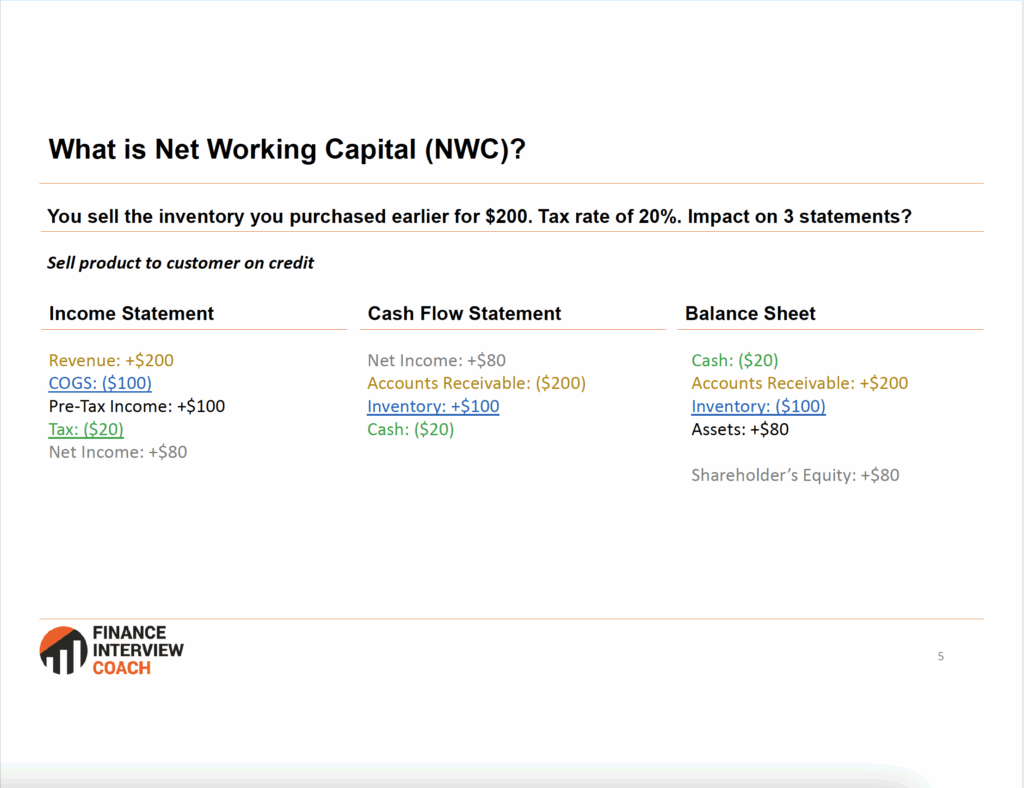

Net Working Capital Schedule

Net Working Capital (NWC) plays a key role in understanding a company’s operational efficiency and its impact on cash flow. This lesson explains how to build and interpret an NWC schedule, why certain items are excluded, and how changes in working capital affect valuation and transaction modeling in investment banking.

In this Lesson:

- Definition: Snapshot of a company’s assets, liabilities, and equity at a point in time.

- NWC Schedule: Tracks operating current assets (AR, Inventory) minus operating current liabilities (AP, Accruals).

- Modeling Purpose: Used to project changes in NWC, which impact cash flow.

- Working Capital Cycle: Shows how efficiently a company converts operations into cash.

- Normalized Adjustments: Removes cash, debt, and financial assets/liabilities to focus on operations.

- IB Relevance: Critical in DCF, M&A, and LBOs when calculating cash impact of operations.

Lesson 4

Balance Sheet - Assets, Liabilities, and Shareholders Equity

The balance sheet is a snapshot of a company’s financial position at a specific point in time—what it owns, what it owes, and what’s left for shareholders. This lesson covers how to read the balance sheet, understand its structure, and see how it connects to the rest of the financial statements.

In the Lesson:

- Assets = Liabilities + Equity: Fundamental accounting equation.

- Current vs. Long-Term: Items split by expected timing (within vs. beyond 12 months).

- Intangibles: Includes goodwill, trademarks – often created via M&A.

- Debt: Short- and long-term borrowings shown on liabilities side.

- Cash: Reflects liquidity available to fund operations or pay down debt.

- IB Relevance: Balance sheet items affect valuation, leverage, and working capital assumptions.

Lesson 5

Net Working Capital - AR, AP, Inventory

Net Working Capital is a key driver of cash flow in financial models, reflecting how a company manages the timing of its receivables, payables, and inventory. This lesson breaks down AR, AP, and Inventory, explains their impact on cash flow, and shows how changes in NWC are used to adjust free cash flow in DCFs and other valuation models.

In this Lesson:

- Definition: NWC = Operating Current Assets – Operating Current Liabilities (excludes cash, debt, and financial items).

- AR (Accounts Receivable): Sales made but not yet collected — an operating asset.

- AP (Accounts Payable): Purchases made but not yet paid – an operating liability.

- Inventory: Goods held for sale – counted as an operating asset.

- Cash Flow Impact: Increases in AR or Inventory use cash; increases in AP free up cash.

- Modeling Note: Track changes in NWC year-over-year to adjust free cash flow.

Lesson 6

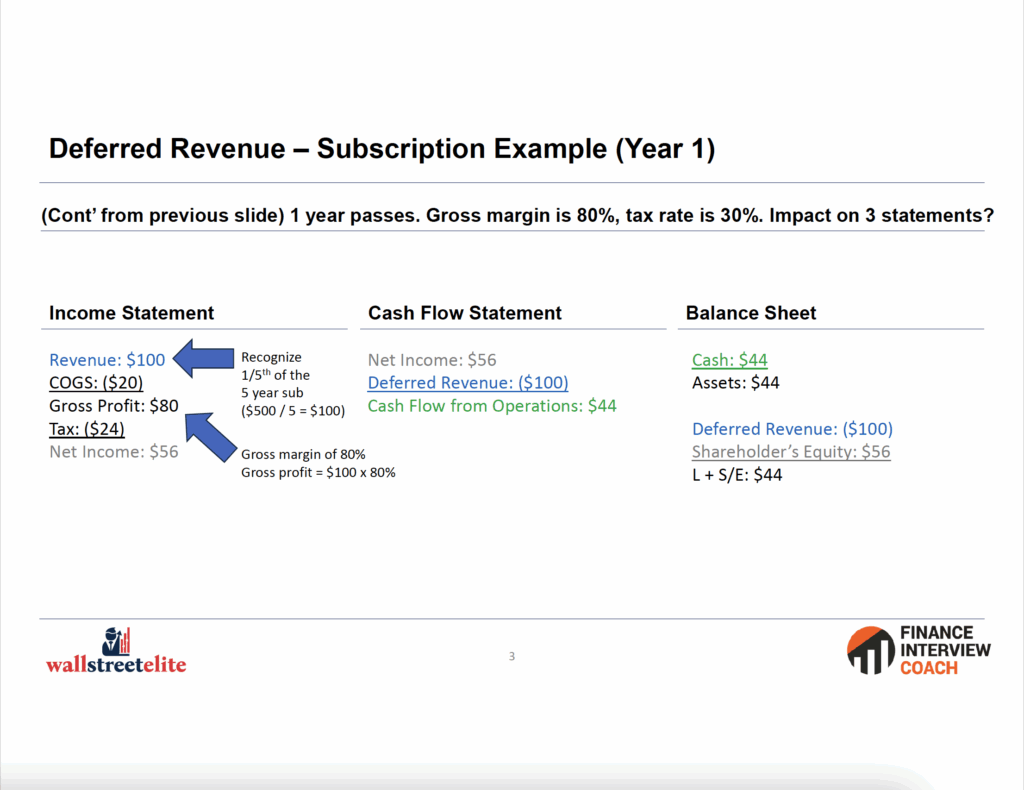

Net Working Capital Continued- Deferred Revenue, Prepaid Expenses, Accrued Expenses

Deferred revenue, prepaid expenses, and accrued expenses are key components of working capital that reflect timing differences between cash and service delivery. This lesson explains how each item functions, how they impact the financial statements, and why they matter when assessing earnings quality and cash flow in investment banking.

In this Lesson:

- Deferred Revenue: Cash collected before service delivered (e.g., subscriptions) — liability.

- Prepaid Expenses: Cash paid for services not yet received — asset.

- Accrued Expenses: Incurred but unpaid — liability (e.g., wages, utilities).

- Recognition Timing: Impacts income statement based on delivery of service or time.

- Balance Sheet Impact: All affect current asset/liability balances and cash flow.

- IB Relevance: Important for working capital, understanding quality of earnings.

Lesson 7

Property Plant and Equipment (Coming Soon)

Property, Plant, and Equipment (PP&E) represents the long-term physical assets that drive a company’s operations, especially in asset-intensive industries. This lesson covers how PP&E is modeled over time, the impact of depreciation and capex, and why it’s crucial for understanding cash flow, valuation, and industry dynamics in investment banking.

In this Lesson:

- Definition: Long-term tangible assets used in operations (factories, machinery, etc.).

- Modeling: PP&E is increased by capex and reduced by depreciation.

- Depreciation: Non-cash expense on the income statement; adds back on cash flow.

- CapEx Forecasting: Often tied to revenue or as a % of sales in modeling.

- PP&E Schedule: Tracks gross PP&E, accumulated depreciation, and net PP&E.

- IB Relevance: Affects D&A assumptions, capex forecasts, and asset-heavy industries.

Lesson 8

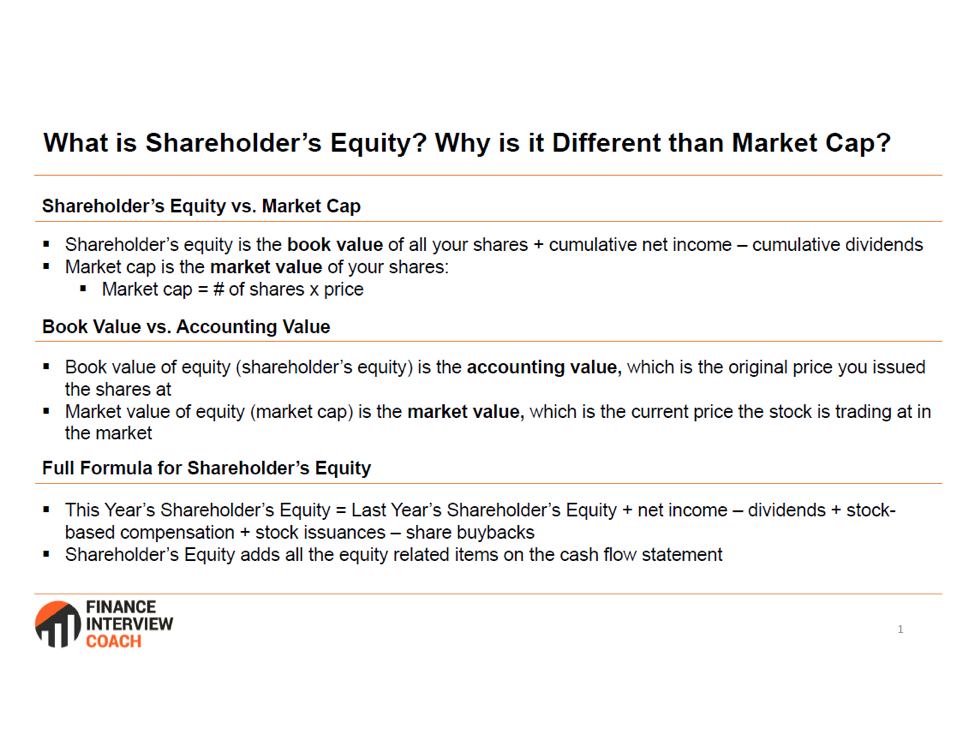

Shareholders Equity (Coming Soon)

Shareholders’ equity represents the ownership value of a company after liabilities are subtracted from assets. This lesson breaks down each component—common stock, APIC, retained earnings, treasury stock, and OCI—and explains how they reflect capital raised, profits retained, and changes in equity over time.

In this Lesson:

- Common Stock: Value of shares issued at par (often minimal).

- Additional Paid-in Capital (APIC): Excess paid over par value in equity raises.

- Retained Earnings: Cumulative net income minus dividends paid.

- Treasury Stock: Repurchased shares — reduces equity.

- OCI (Other Comprehensive Income): Gains/losses not in net income (FX, pensions).

Josh has been a phenomenal mentor of mine since I was in first-year university. His extensive experience in investment banking and private equity made him the perfect interview prep coach, especially since he has gone through the recruiting process himself. In addition, he has a knack for giving intuitive explanations for financial concepts, ensuring that I fully understood the theory as opposed to simply memorizing the answers to a list of interview questions. His friendly disposition also made him a pleasure to interact with. In the end, I was able to secure an investment analyst position on the buy-side upon graduation. I definitely would not have been able to get there without his help, so many thanks to Josh for helping me jumpstart my career!

HS

Start your IB prep today.

Don’t wait to get ahead—start your IB prep today.