Module 6: M&A

Recruiting | Behaviorals | Accounting | Enterprise Value / Comparables | DCF | M&A | LBO| Market questions | Brain teasers

Understanding the Strategy, Structure, and Impact of Deals

Mergers and Acquisitions (M&A) are a cornerstone of investment banking, and this module gives you a clear, practical understanding of how deals are structured, financed, and analyzed. You’ll learn the strategic reasons behind acquisitions, the difference between cost and revenue synergies, and how to distinguish between deal types like horizontal mergers, LBOs, and bolt-ons. We walk through how deals are financed with cash, stock, or debt, and compare their impacts on ownership and risk. You’ll also master accretion/dilution analysis using both quick screening and full merger model methods. Whether you’re on the buy-side or sell-side, this module will sharpen your ability to break down and evaluate real-world transactions with clarity and confidence.

Lesson 1

Strategic rationale for M&A deals (Coming Aug 12)

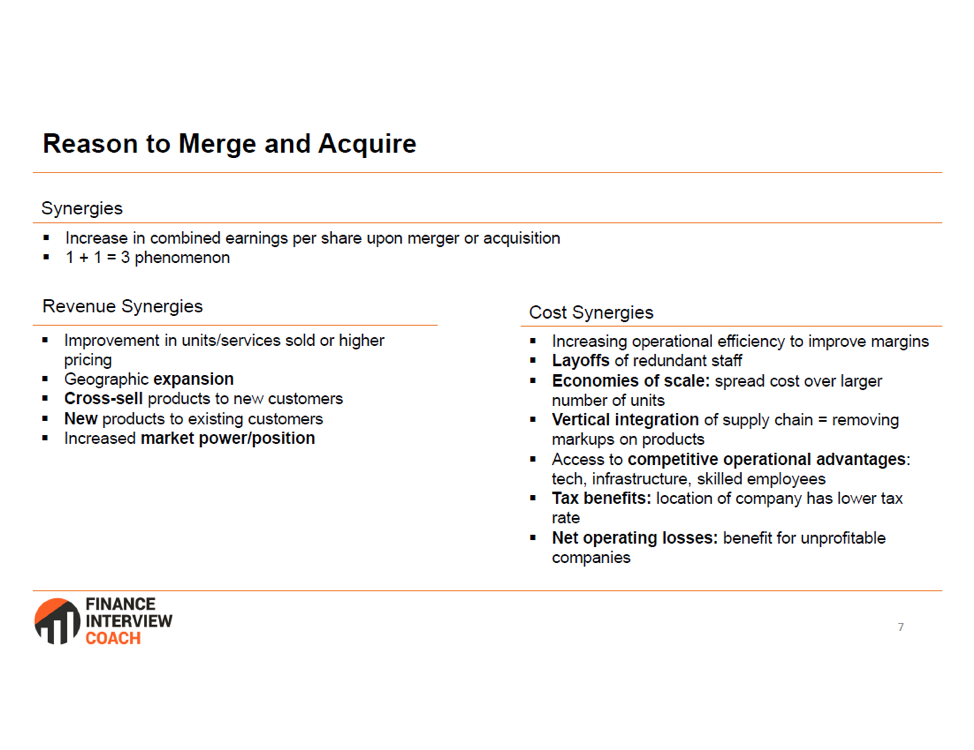

M&A deals are often driven by strategic goals that go beyond financial metrics, aiming to strengthen a company’s long-term position. This lesson explores common rationales like synergies, market expansion, product diversification, and gaining competitive edge through scale, talent, or technology.

In this lesson:

- Synergies: Cost savings or revenue gains from combining operations.

- Market Expansion: Enter new geographies, customer segments, or verticals.

- Product Diversification: Broaden product or service offerings.

- Scale and Efficiency: Gain size to improve margins and competitiveness.

- Talent or IP Acquisition: Access key talent, patents, or proprietary tech.

- Competitive Advantage: Eliminate a rival or strengthen market position.

Lesson 2

Why do most M&A deals fail (Coming Aug 16)

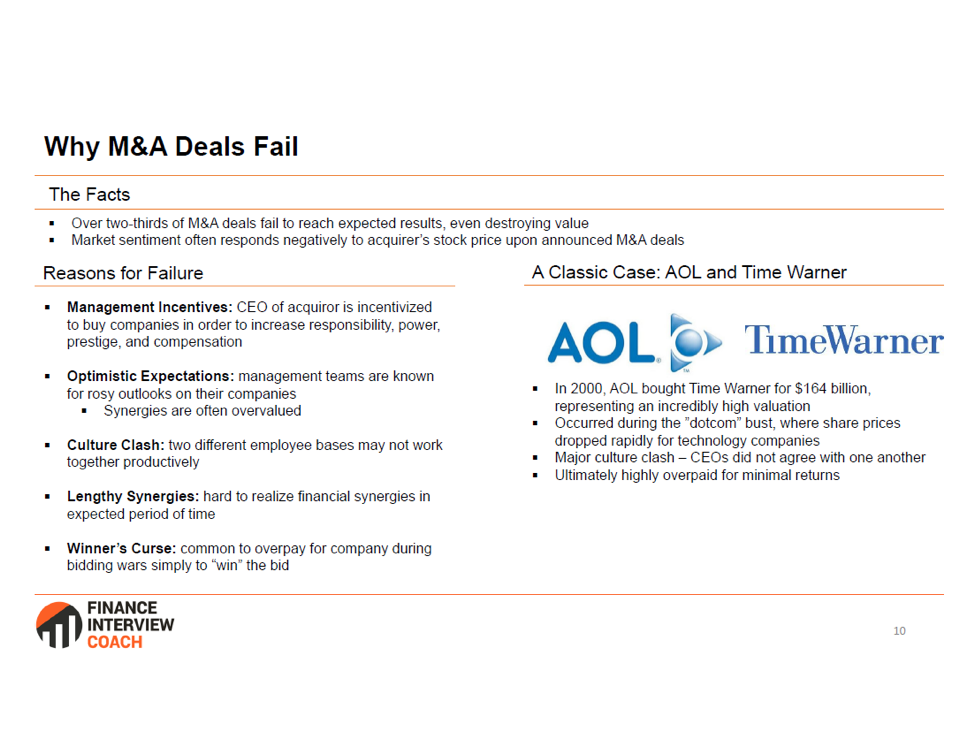

Most M&A deals fail because the promised value isn’t realized—often due to overpaying, poor integration, or unrealistic synergy expectations. This lesson covers the common pitfalls, from strategic misalignment and leadership distraction to cultural clashes and employee turnover.

- Overpaying: Paying too high a premium reduces long-term value.

- Integration Issues: Poor cultural or operational integration disrupts performance.

- Overestimated Synergies: Cost savings or revenue boosts fail to materialize.

- Strategic Misalignment: Deal doesn’t fit long-term business goals.

- Management Distraction: Leadership focus shifts from core operations.

- Employee Turnover: Key talent may leave due to uncertainty or culture clash.

Lesson 3

Financing an M&A deal (Coming Aug 14)

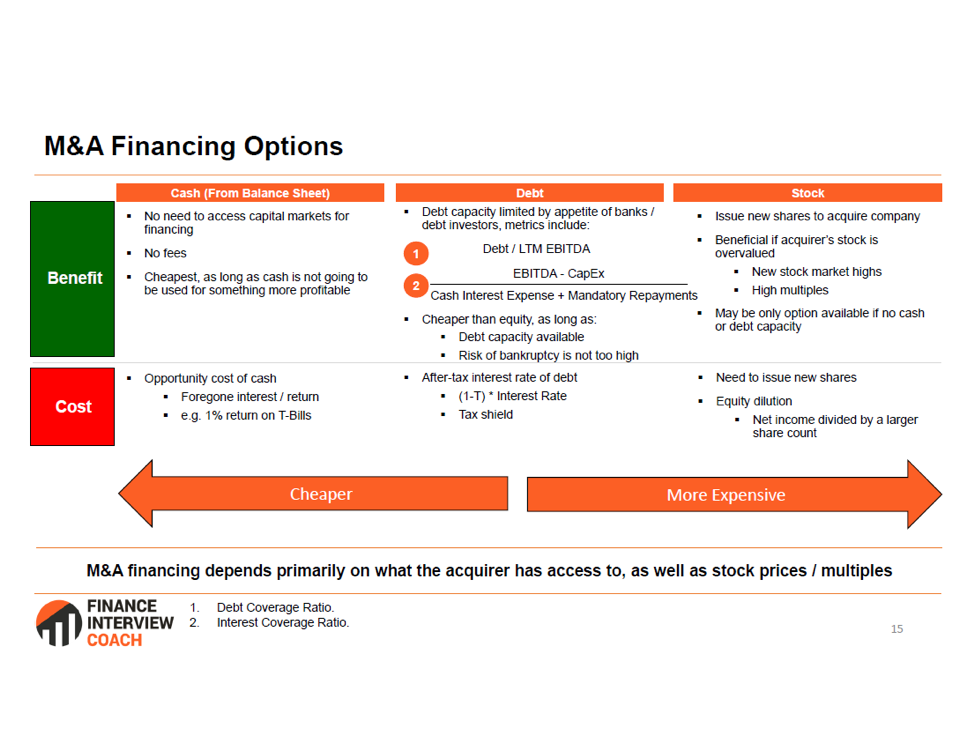

M&A deals can be financed through cash, stock, debt, or a mix—each with trade-offs in cost, dilution, and risk. This lesson explores common structures like seller financing and earnouts, which help bridge valuation gaps and align incentives between buyer and seller.

In this lesson:

- Cash: Simplest method; no dilution but reduces liquidity or adds debt.

- Stock: Buyer issues shares; preserves cash but dilutes ownership.

- Debt: Increases leverage; interest expense affects earnings and risk.

- Seller Financing: Seller provides a loan or deferred payment structure.

- Earnouts: Future payments tied to performance targets; aligns incentives.

Lesson 4

Revenue vs. cost synergies (Coming Aug 19)

Synergies are a key driver of M&A value, but not all synergies are created equal. This lesson breaks down cost synergies—like eliminating redundancies or improving operations—and revenue synergies from cross-selling or market expansion, highlighting why cost synergies are generally more certain and quicker to realize.

In this lesson:

- Cost Synergies – Redundancies: Savings from eliminating redundancies (e.g., headcount, SG&A, supply chain), economies of scale.

- Cost Synergies – Improvements: operational improvements, applying best practices, increased bargaining power

- Revenue Synergies: Gains from cross-selling, pricing power, or market expansion.

- Certainty: Cost synergies are easier to estimate and realize.

- Timing: Cost synergies often realized faster post-close; revenue synergies take longer.

Lesson 5

Types of M&A deals (Coming Aug 26)

M&A deals come in various forms depending on strategic goals, industry position, and structure. This lesson covers key deal types—horizontal, vertical, conglomerate, bolt-on, buyout, and merger of equals—each with distinct implications for integration, control, and value creation.

In this lesson:

- Horizontal: Merger with a direct competitor to gain market share.

- Vertical: Acquisition up or down the supply chain (e.g., supplier or distributor).

- Conglomerate: Combination of unrelated businesses to diversify risk.

- Bolt-On / Add-On: Smaller acquisition by a larger platform to expand offerings.

- Buyout / LBO: Acquisition using significant debt, often by private equity.

- Merger of Equals: Two similarly sized firms combine, typically via stock swap.

Lesson 6

Cash vs. stock deals (Coming Aug 27)

Cash and stock are the two primary ways to structure M&A payments, each with trade-offs in certainty, risk, and dilution. This lesson explains when to use cash vs. stock, and how each impacts shareholders, deal structure, and post-merger dynamics.

In this lesson:

- Cash Deals: Buyer pays in cash; target shareholders exit immediately.

- Stock Deals: Buyer offers shares; target shareholders become part-owners.

- Certainty: Cash offers more deal certainty; stock depends on buyer’s valuation.

- Risk Sharing: Stock shifts more risk to target shareholders post-deal.

- Dilution: Stock deals dilute buyer’s existing shareholders; cash does not.

- Use Case: Cash for smaller or accretive deals; stock for large or strategic mergers.

Lesson 7

Accretion / dilution - earnings yield method

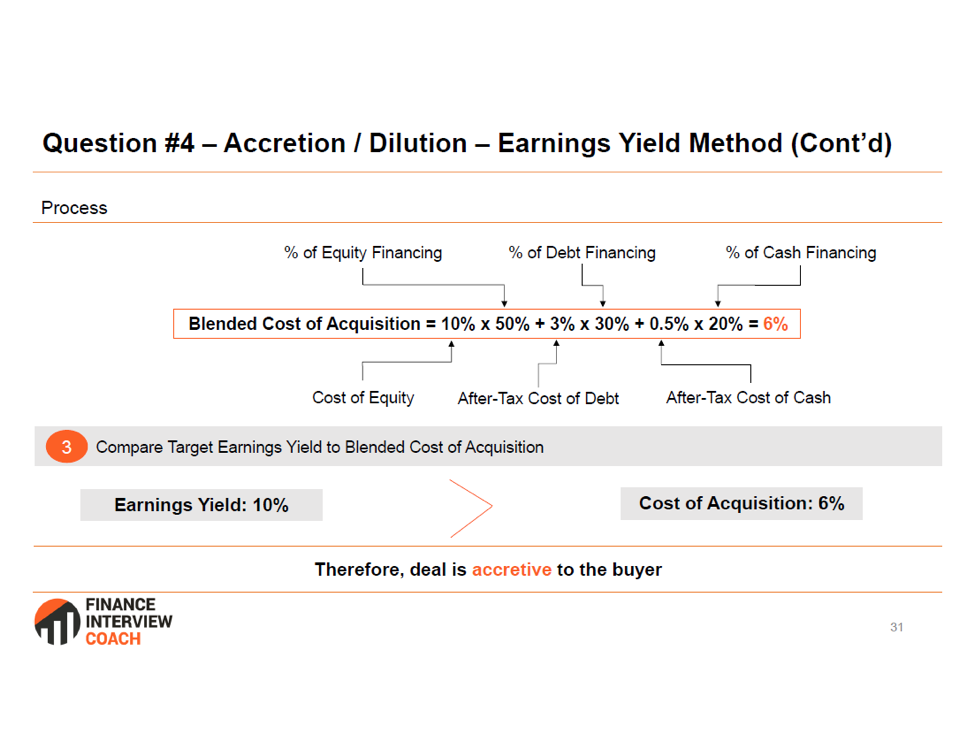

Accretion/dilution analysis quickly assesses whether an M&A deal will increase or decrease the buyer’s earnings per share. By comparing the target’s earnings yield to the buyer’s cost of capital, it offers a fast screening tool—but doesn’t account for synergies or show exact dollar impact.

In this lesson:

- Core Concept: Compares target’s earnings yield to buyer’s cost of capital

- Earnings Yield: Reciprocal of P / E ratio

- Accretion: If target’s earnings yield > buyer’s cost of capital, deal is accretive

- Quick Screening Tool: Used for fast, rough estimates before full merger model.

- Limitations: Ignores synergies, does not produce $ amount of accretion / dilution

Lesson 8

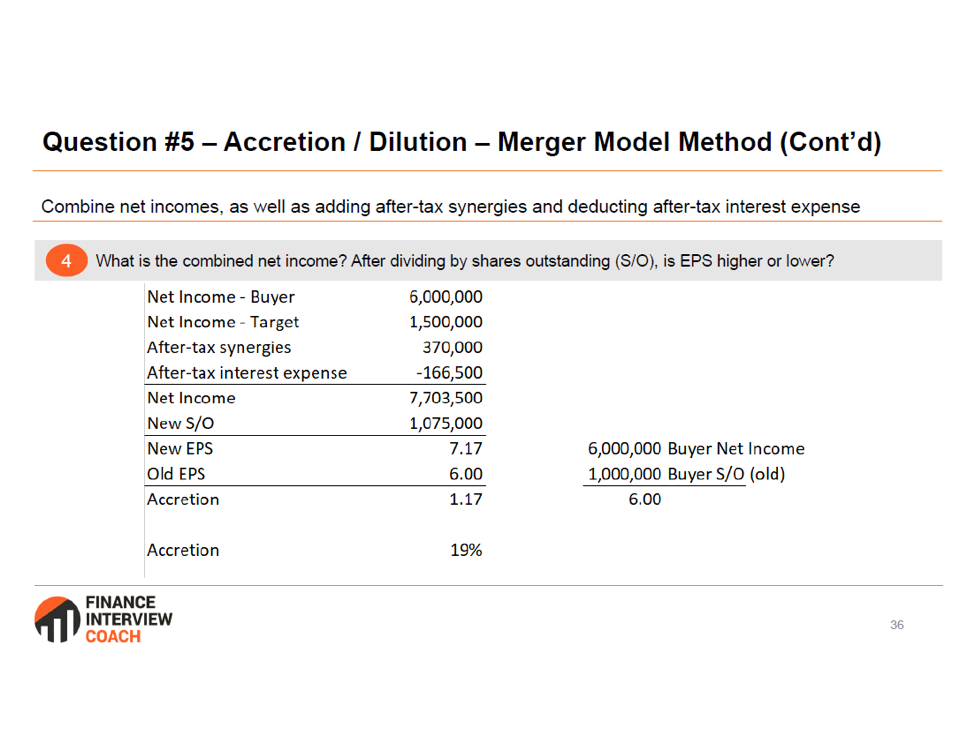

Accretion / dilution - merger model method

The merger model method calculates accretion or dilution by combining the buyer’s and target’s net incomes, adjusting for synergies and financing, and dividing by the new share count to get pro forma EPS. It provides a more accurate picture of a deal’s short-term impact on earnings, factoring in the effects of stock dilution, interest expense, and synergies.

In this lesson:

- Definition: Measures whether a deal increases (accretive) or decreases (dilutive) the buyer’s EPS.

- Key Inputs: Buyer and target net income, deal structure (cash vs. stock vs. debt), synergies.

- Pro Forma EPS: Combine net incomes, adjust for synergies and financing, then divide by new share count.

- Stock Impact: Stock increases share count (dilution risk); debt and cash deducts interest expense or lost interest income

- Use Case: Used to assess short-term profitability of a deal

Josh is a great mentor and was a crucial component of my career development early on, and the guidance he provided me on financial modeling and LBO modeling gave me a step up in both recruiting and work. He is extremely competent with regards to teaching financial concepts for individuals both new and familiar with finance, and is always happy to share honest advice. They are both genuinely care about your success and I would recommend him to anyone interested in developing the necessary skills to pursuing a career in finance early on.

Daniel Cheung

Investment Analyst at Highbridge Capital

Start your IB prep today.

Don’t wait to get ahead—start your IB prep today.