Module 7: LBO

Recruiting | Behaviorals | Accounting | Enterprise Value / Comparables | DCF | M&A | LBO| Market questions | Brain teasers

LBOs Demystified: Modeling, Mechanics & Maximizing Returns

Leveraged Buyouts (LBOs) are a fundamental concept in private equity and advanced investment banking interviews. This module gives you a deep understanding of how LBOs work, why they’re used, and how to analyze them. You’ll learn how private equity firms use debt to amplify returns, the ideal characteristics of an LBO target, and how capital is structured through senior and junior debt. From simplified Paper LBOs to full Excel models, this module breaks down each step—from entry multiples and free cash flow projections to debt paydown and exit IRR. You’ll also explore key topics like covenants, PIK interest, and how small changes in assumptions affect investor returns. If you’re targeting PE roles or modeling-focused banking positions, this is essential prep.

Lesson 1

Purpose of debt in an LBO (Coming Aug 17)

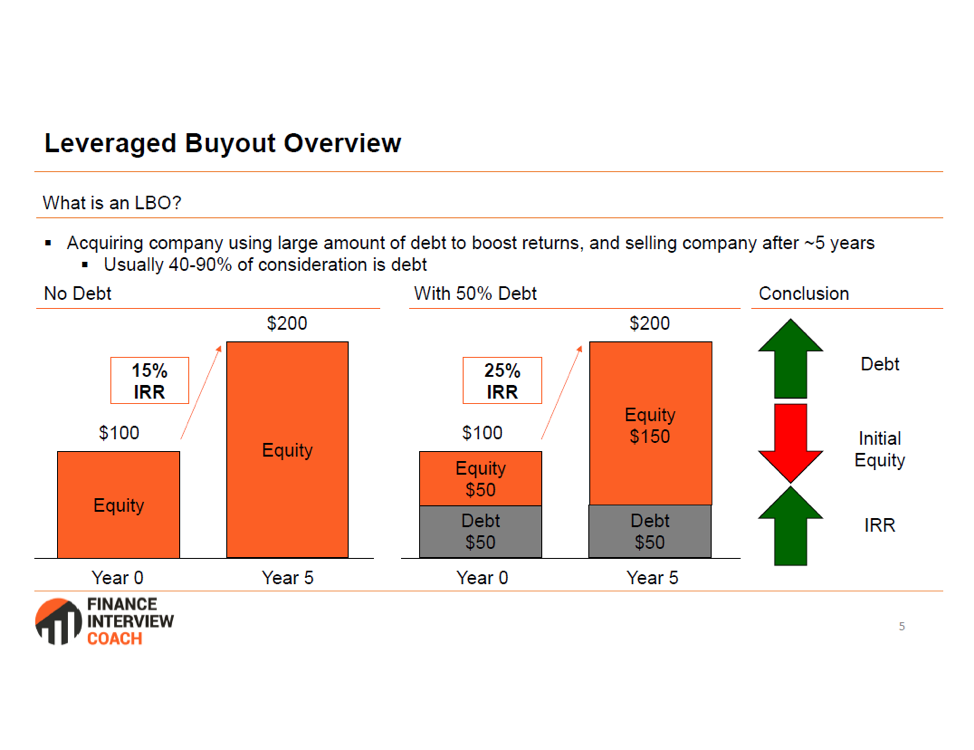

In a leveraged buyout (LBO), debt is used to reduce the equity investment and amplify returns for the sponsor. It provides tax benefits through interest deductibility and boosts IRR as the debt is paid down over time.

In this lesson:

- Maximize Returns: Debt amplifies equity returns if the deal performs well.

- Lower Equity Requirement: Reduces upfront capital needed from the sponsor.

- Tax Shield: Interest on debt is tax-deductible

- Debt Paydown: Enhances IRR through debt paydown and multiple expansion.

Lesson 2

Characteristics of an ideal LBO target (Coming Aug 15)

An ideal LBO target has stable cash flows, low capital expenditure needs, and a strong market position to support high debt levels. Additional appeal comes from growth potential, operational improvement opportunities, and a purchase price that allows for attractive returns.

In this lesson:

- Stable Cash Flows: Predictable earnings to support debt repayment.

- Low CapEx Needs: Minimizes cash drain, boosting free cash flow.

- Strong Market Position: Competitive edge or pricing power reduces risk.

- Growth Opportunities: Multiple organic and inorganic opportunities for growth

- Opportunity for Efficiency Gains: Room for margin expansion or cost cuts.

- Valuation: Attractive valuation and returns

Lesson 3

Senior vs. Junior Debt (Coming Aug 18)

Senior and junior debt differ in risk, repayment priority, and cost—senior debt is secured, lower-risk, and repaid first, while junior debt is subordinated and carries higher interest rates. In LBOs, senior debt provides the core financing, while junior debt adds flexibility to complete the capital stack and boost potential returns.

In this lesson:

- Seniority in Capital Structure: Senior debt gets repaid first in liquidation; junior ranks lower.

- Collateral: Senior is often secured by assets; junior is usually unsecured or subordinated.

- Interest Rates: Senior has lower floating rates due to lower risk; junior demands higher fixed rates.

- Covenants: Senior debt has stricter terms and maintenance covenants.

- Alternative Structures: Convertible debt and preferred equity can be used to increase returns.

- Use in LBOs: Senior debt forms the base layer; junior debt fills funding gaps with flexibility.

Lesson 4

Walkthrough of LBO model (Coming Aug 13)

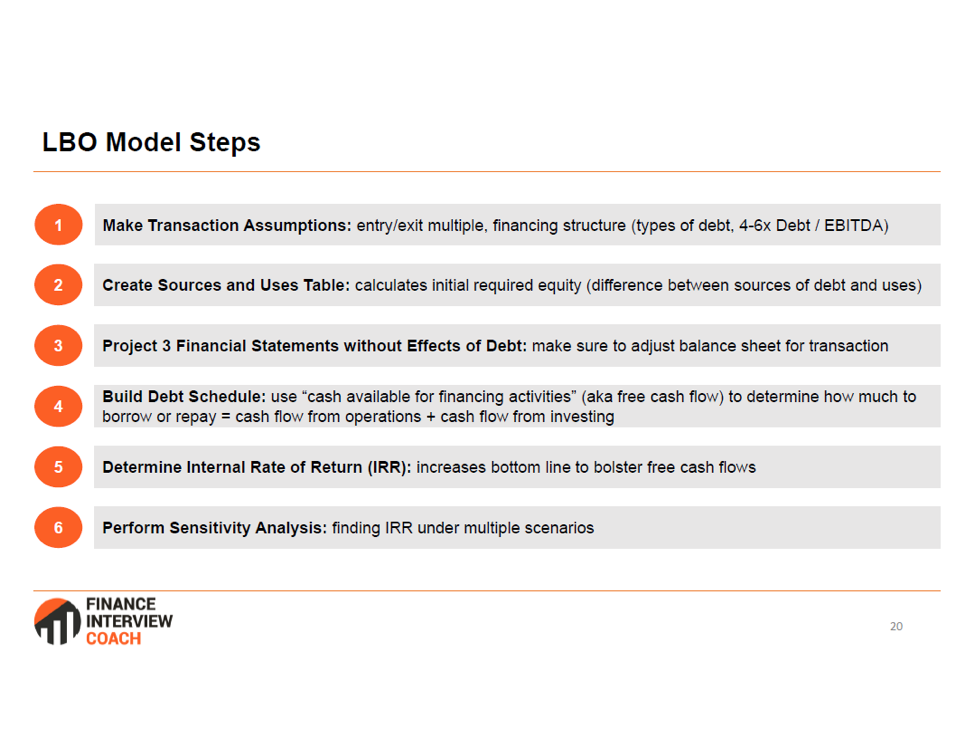

An LBO model evaluates the returns from acquiring a company primarily using debt, with a focus on cash flow and leverage. This lesson walks through key steps: setting assumptions, projecting financials, modeling debt paydown, and calculating IRR and MOIC at exit.

In this lesson:

- Assumptions: Set entry and exit multiple, debt multiple, operating assumptions (revenue growth, margins).

- Sources & Uses: Detail where capital comes from (sources) and how it’s spent (uses) to find initial required equity.

- Financial Projections: Forecast income statement, cash flow and balance sheet over ~5 years.

- Debt Schedule: Model revolver usage. interest, and principal repayments

- Exit Assumptions: Apply exit multiple to final-year EBITDA to estimate sale proceeds.

- IRR & MOIC: Calculate investor returns based on entry vs. exit equity value.

Lesson 5

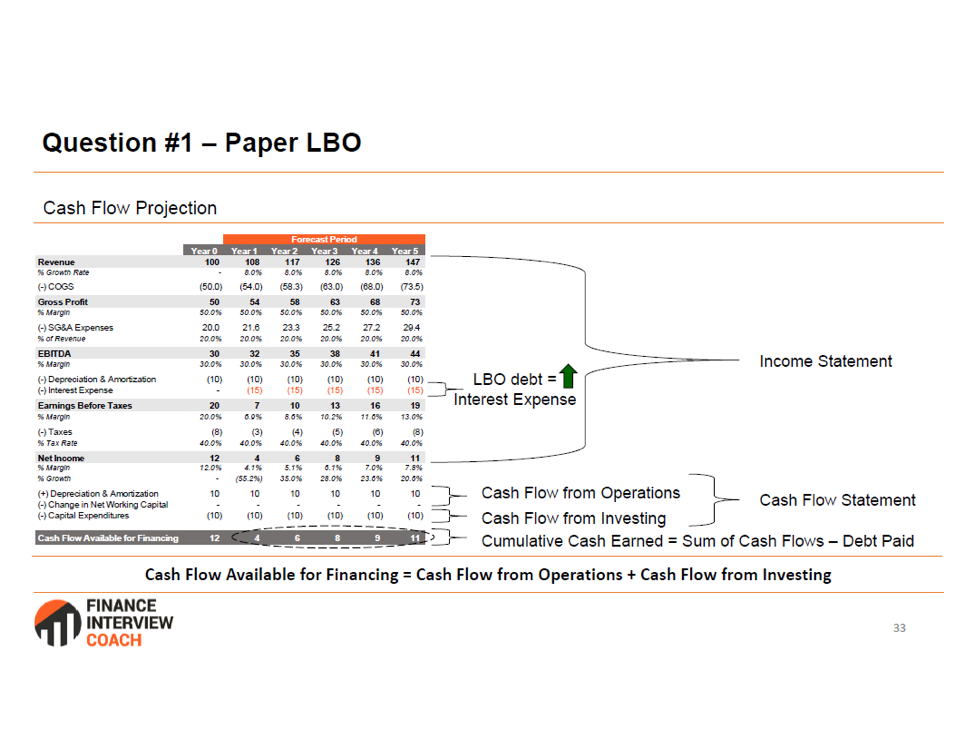

Paper LBO - simplified (Coming Aug 3)

A Paper LBO is a simplified, pen-and-paper version of a full LBO model used to test core concepts quickly. This lesson walks through basic assumptions, EBITDA growth, debt paydown, and exit valuation to estimate investor returns using IRR and MOIC.

In this lesson:

- Step 1 – Entry Assumptions: Assume entry, exit, and debt multiple

- Step 2 – EBITDA: Project EBITDA over 5 years

- Step 3 – Debt Paydown: Given annual LFCF; calculate cumulative debt repayment.

- Step 4 – Exit Value: Apply exit multiple to year 5 EBITDA to get sale proceeds.

- Step 5 – IRR/MOIC: Calculate return by comparing entry vs. exit equity value using rule of 72

Lesson 6

Paper LBO - complete (Coming Aug 4)

A complete Paper LBO builds on the simplified version by incorporating annual free cash flow to more accurately model debt paydown over time. This lesson walks through entry assumptions, EBITDA growth, annual LFCF, cumulative debt repayment, and exit value to estimate returns—or reverse-engineer the entry price for a target IRR.

In this lesson:

- Step 1 – Entry Assumptions: Assume entry, exit, and debt multiple

- Step 2 – EBITDA: Project EBITDA over 5 years

- Step 3 – LFCF: Calculate LFCF each year (or use an average)

- Step 3 – Debt Paydown: Calculate cumulative debt repayment (sum of annual LFCF)

- Step 4 – Exit Value: Apply exit multiple to year 5 EBITDA to get sale proceeds using rule of 72

Variation: calculate implied entry multiple for a given IRR

Lesson 7

Covenants (Coming Aug 21)

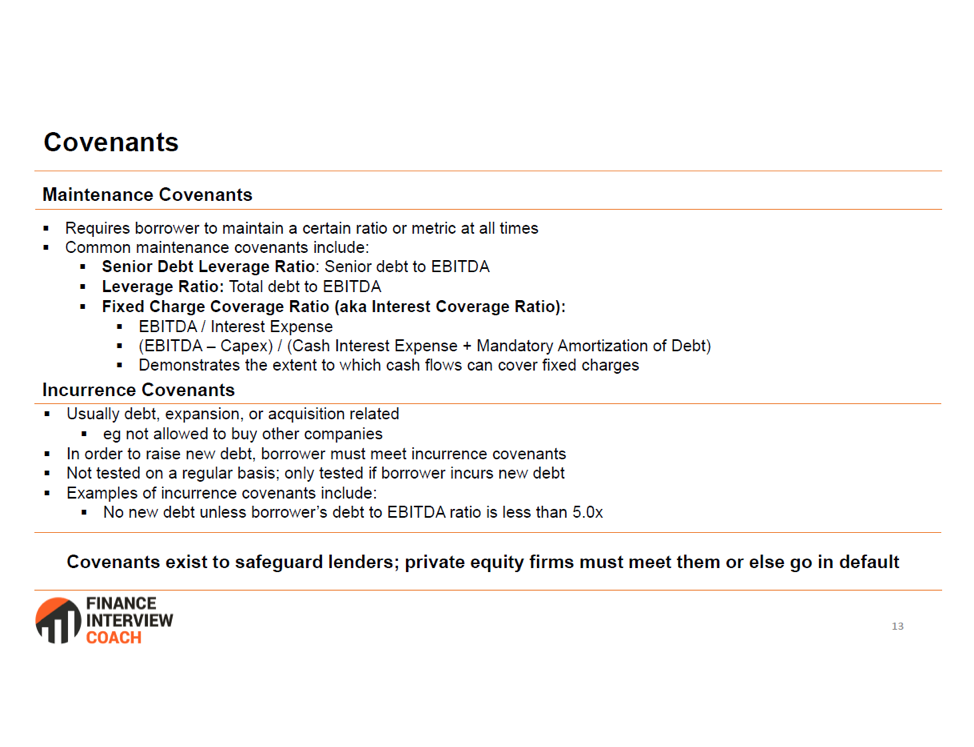

Covenants are loan agreement terms that restrict borrower behavior to protect lenders and ensure financial discipline. This lesson explains the difference between maintenance and incurrence covenants, their role in LBOs, and the consequences of breaching them.

In this lesson:

- Definition: Rules in loan agreements that protect lenders by limiting borrower actions.

- Maintenance Covenants: Ongoing financial tests (e.g. Debt/EBITDA) tested quarterly.

- Incurrence Covenants: Restrictions on specific actions like taking on new debt or paying dividends.

- Purpose: Reduce lender risk by ensuring financial discipline and early warning of distress.

- Consequences of Breach: May lead to default, renegotiation, or accelerated repayment.

- LBO Relevance: Key in structuring debt and assessing the viability of a deal

Josh has been a phenomenal mentor of mine since I was in first-year university. His extensive experience in investment banking and private equity made him the perfect interview prep coach, especially since he has gone through the recruiting process himself. In addition, he has a knack for giving intuitive explanations for financial concepts, ensuring that I fully understood the theory as opposed to simply memorizing the answers to a list of interview questions. His friendly disposition also made him a pleasure to interact with. In the end, I was able to secure an investment analyst position on the buy-side upon graduation. I definitely would not have been able to get there without his help, so many thanks to Josh for helping me jumpstart my career!

HS

Investment Analyst at Mackenzie Investments

Start your IB prep today.

Don’t wait to get ahead—start your IB prep today.