Module 5: DCF

Recruiting | Behaviorals | Accounting | Enterprise Value / Comparables | DCF | M&A | LBO| Market questions | Brain teasers

Discounted Cash Flow: Valuing Businesses from First Principles

Module 5 provides a deep dive into the Discounted Cash Flow (DCF) method—one of the most fundamental valuation techniques in investment banking. You’ll start with the basics of the time value of money and build toward complete mastery of the DCF process, from forecasting free cash flow to calculating WACC, beta, and terminal value. Each lesson breaks down critical inputs, modeling logic, and valuation intuition. Whether you’re preparing for technical interviews or building real models, this module gives you a step-by-step understanding of how intrinsic value is derived — and how every assumption shapes your result.

Lesson 1

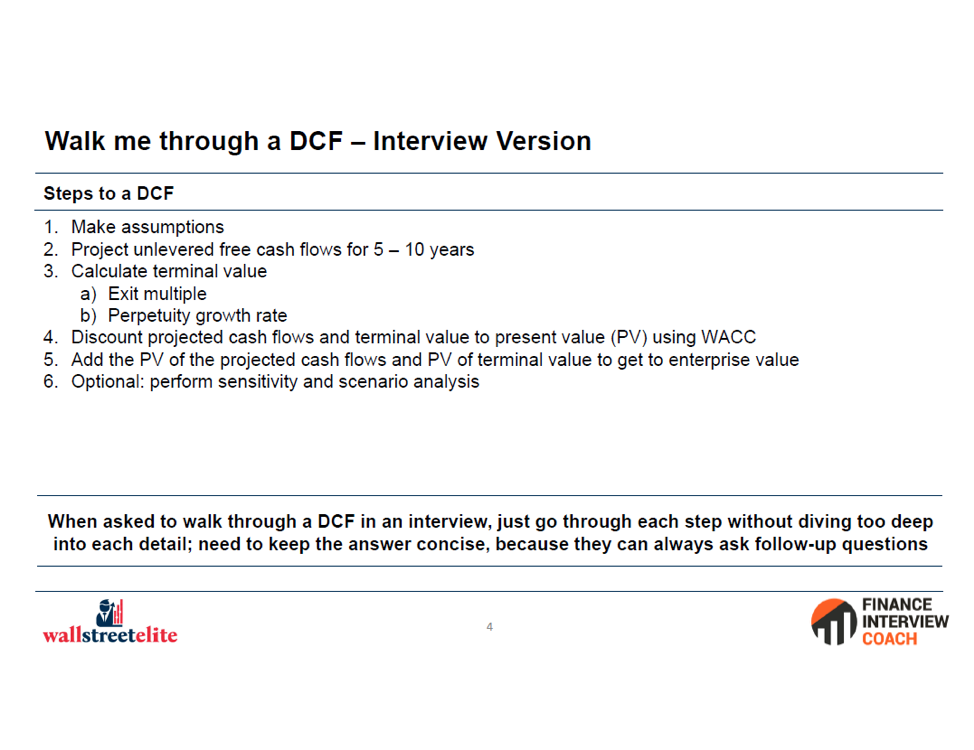

Walkthrough of a DCF model

The DCF is one of the most rigorous and widely used valuation methods in investment banking, focused on estimating a company’s intrinsic value based on future cash flows. This lesson walks through each step of the model—from assumptions to sensitivity analysis.

In this lesson

- Assumptions: model assumptions (WACC, terminal value), operating assumptions (revenue growth, margins)

- Project Free Cash Flow: Forecast unlevered FCF over ~5–10 years using revenue, margins, depreciation, capex, and working capital.

- Calculate Terminal Value: Use exit multiple or perpetuity growth rate to estimate value beyond forecast.

- Discount Rate (WACC): Reflects time value of money and business risk.

- Enterprise Value: Discount FCFs and terminal value back to present using WACC.

- Scenario and Sensitivity Analysis: Subtract net debt and other claims from EV.

Lesson 2

Unlevered free cash flow (Coming Aug 2)

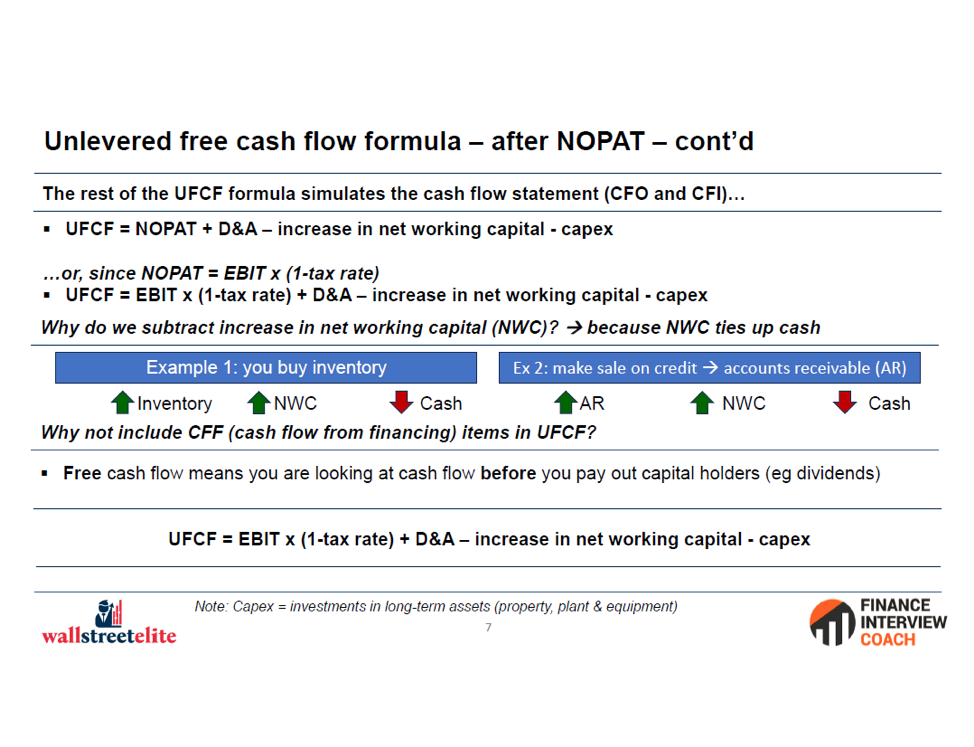

Unlevered free cash flow represents the cash available to all investors—both debt and equity—before interest payments are made. It’s calculated by starting with EBIT, applying taxes, adjusting for capex and working capital, and adding back non-cash expenses like depreciation.

In this lesson:

- Core Definition: Cash flow available to all investors (debt + equity) before interest.

- Starting Point: Begin with EBIT (or EBITDA minus D&A).

- Less Taxes: Apply taxes on EBIT to get NOPAT (Net Operating Profit After Tax).

- Adjust for CapEx & Working Capital: Subtract capital expenditures and changes in working capital.

- Add Back Non-Cash Items: Add D&A and other non-cash expenses.

- Use in Valuation: Central input for DCF and enterprise value calculations.

Lesson 2

Levered free cash flow (Coming Aug 2)

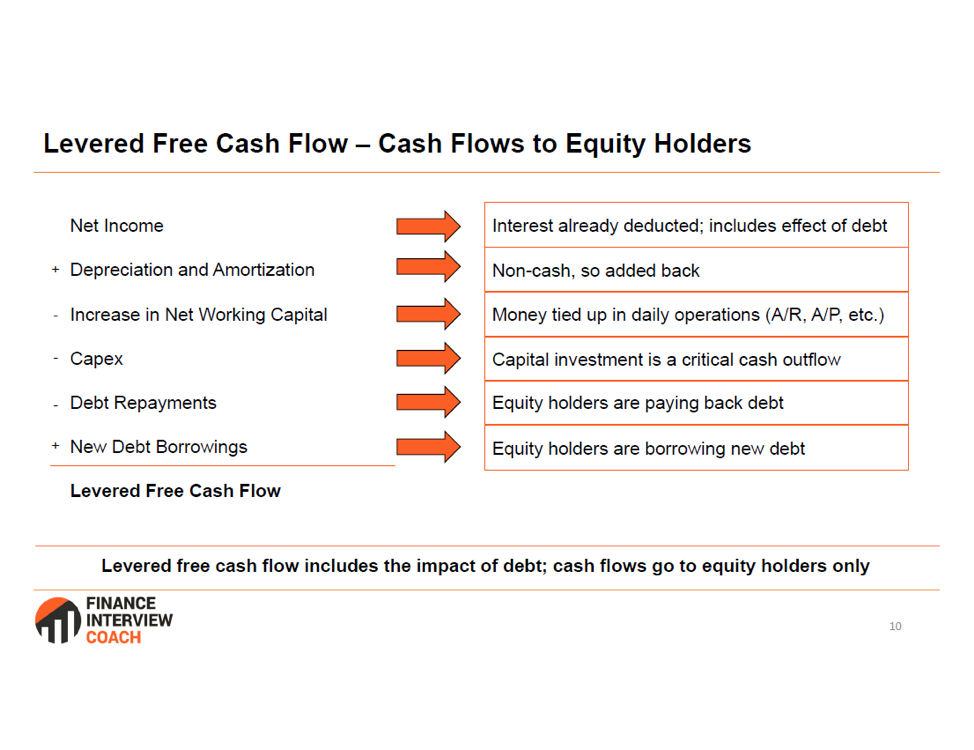

Levered free cash flow is the cash available to equity holders after interest expenses and debt repayments have been made. It starts with net income, adds back non-cash items, adjusts for capex and working capital, and subtracts mandatory debt payments to reflect true cash flow to shareholders.

In this lesson:

- Core Definition: Cash flow available to equity holders after interest and debt payments.

- Starting Point: Begin with net income from the income statement.

- Add Back Non-Cash Items: Include D&A and other non-cash expenses.

- Adjust for CapEx & Working Capital: Subtract capital expenditures and changes in working capital.

- Subtract Mandatory Debt Repayment: Reflects actual cash left for shareholders.

- Use in Valuation: Used in equity value DCF models and dividend discount approaches.

Lesson 3

WACC (Coming Aug 6)

WACC (Weighted Average Cost of Capital) represents the average return required by both debt and equity investors, weighted by the company’s capital structure. It’s used as the discount rate in unlevered DCF models to calculate enterprise value, combining the cost of equity and after-tax cost of

debt.

In this lesson:

- Core Concept: Average return required by all capital providers (debt + equity).

- Formula: WACC = (E/V × Cost of Equity) + (D/V × After-Tax Cost of Debt).

- Cost of Equity: Represents the return that equity investors require to compensate them for the risk

- Cost of Debt: Based on yield to maturity or interest rate on new debt, adjusted for taxes.

- Capital Structure Weights: Based on optimal long-term capital structure

- Use in Valuation: Used as the discount rate in unlevered DCFs to calculate enterprise value.

Lesson 4

Cost of equity (Coming Aug 7)

Cost of equity reflects the return required by shareholders and rises as a company takes on more debt due to increased financial risk. While moderate debt can lower WACC through tax benefits and cheaper capital, too much debt raises default risk and equity cost, creating a U-shaped WACC curve with an optimal capital structure.

In this lesson:

- Debt Is Cheaper: Replacing equity with debt can lower WACC early on.

- Tax Benefit: Interest is tax-deductible, further lowering effective debt cost.

- Equity Gets Riskier: More debt means higher risk for equity, raising its cost.

- Default Risk Rises: Too much debt increases bankruptcy risk, raising overall WACC.

- WACC Curve Is U-Shaped: WACC falls, then rises as debt increases.

- Optimal Mix: There’s a sweet spot where WACC is minimized with balanced debt/equity.

Lesson 5

Terminal value (Coming Aug 9)

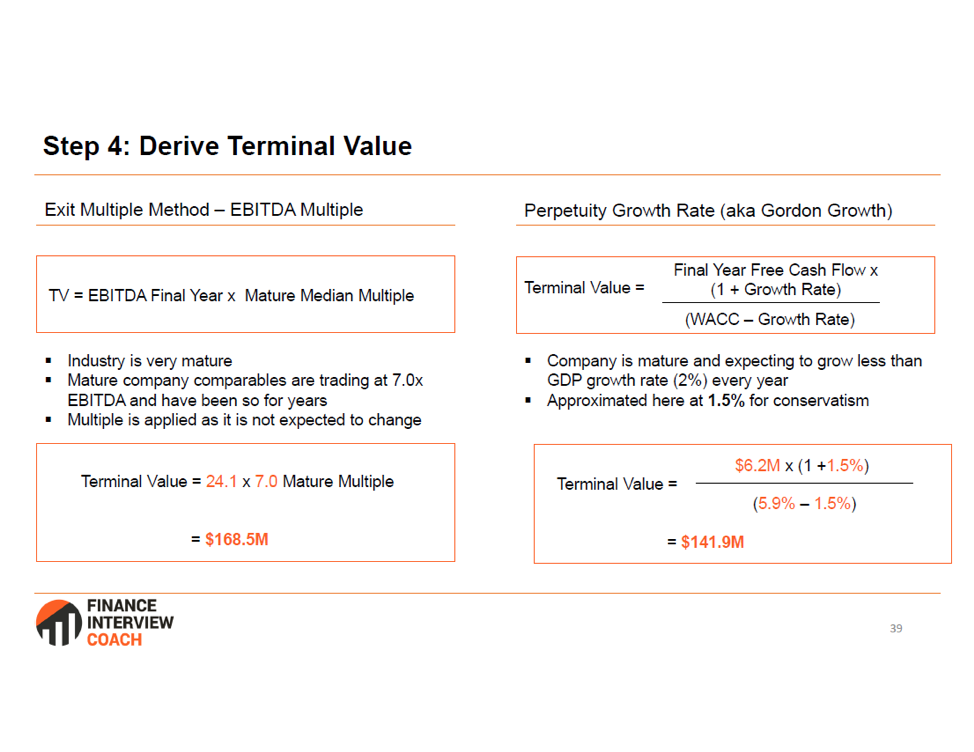

Terminal value estimates the worth of a business beyond the explicit forecast period in a DCF and often accounts for the majority of the total valuation. It’s calculated using either the exit multiple method or the Gordon Growth model, then discounted back to present using WACC.

In this lesson:

- Definition: Captures the value of a business beyond the projection period in a DCF.

- Two Methods: Use either Exit Multiple or Gordon Growth (Perpetuity) method.

- Exit Multiple: Apply a market-based multiple (e.g. EV/EBITDA) to final year metric.

- Gordon Growth: TV = Final Year FCF × (1 + g) / (WACC – g).

- Importance: Often makes up 60–80% of total DCF valuation.

- Discounting: Bring back to present value using WACC.

Lesson 6

Beta and beta comps (Coming Aug 11)

Beta measures a stock’s volatility relative to the market and is a key input in calculating the cost of equity through CAPM. In valuation, analysts use unlevered betas from comparable companies and re-lever them based on the target company’s capital structure to estimate a more accurate beta.

In this lesson:

- Beta Definition: Measures a stock’s volatility relative to the overall market

- Use in CAPM: Key input to calculate cost of equity in WACC.

- Raw vs. Adjusted Beta: Raw beta from regression; adjusted beta (e.g., Bloomberg) trends toward 1.

- Levered vs. Unlevered: Levered beta reflects a firm’s capital structure; unlevered strips out debt impact.

- Beta Comps: Median unlevered betas of peer companies to estimate a reliable beta.

- Re-Levering: Apply target company’s capital structure to peer average beta using relevering formula.

Lesson 7

Cost of debt (Coming Aug 20)

Cost of debt represents the effective interest rate a company pays on its borrowings and is a key component of WACC. It can be estimated using recent bond yields, comparable company debt, SEC filings, or by applying a credit spread to a benchmark rate based on the company’s credit profile.

In this lesson:

- Learn how to find cost of debt using one of the common methods

- Filings: 10K, notes to financial statements

- Yields of recently issued bonds

- Bond yields of comps

- Apply spread to benchmark rate based on credit rating

- Create synthetic credit rating

Lesson 8

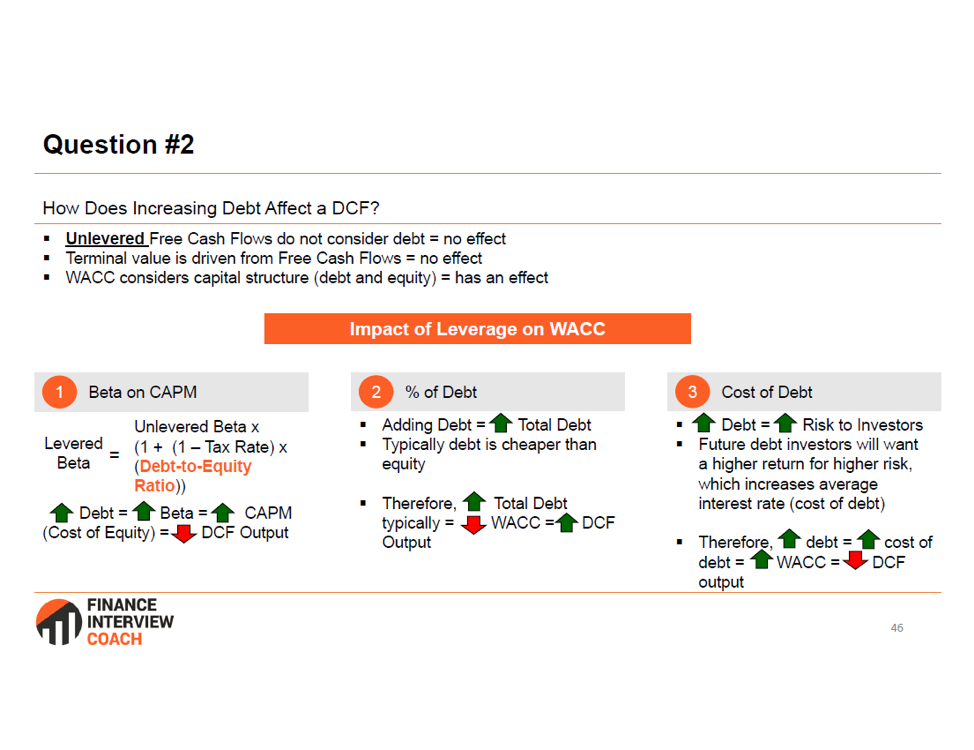

How does increasing debt impact WACC (Coming Aug 25)

Increasing debt can initially lower WACC due to its lower cost and tax-deductible interest, making it cheaper than equity. However, beyond a certain point, added debt raises default risk and makes equity riskier, causing both costs to rise and pushing WACC back up—resulting in a U-shaped curve with an optimal capital structure.

In this lesson:

- Debt Is Cheaper: Replacing equity with debt can lower WACC early on.

- Tax Benefit: Interest is tax-deductible, further lowering effective debt cost.

- Equity Gets Riskier: More debt means higher risk for equity, raising its cost.

- Default Risk Rises: Too much debt increases bankruptcy risk, raising overall WACC.

- WACC Curve Is U-Shaped: WACC falls, then rises as debt increases.

- Optimal Mix: There’s a sweet spot where WACC is minimized with balanced debt/equity.

Josh has been invaluable in helping me improve my financial modeling skills and sharpen my understanding of material details in private equity transactions. Josh is a great teacher and is able to effectively communicate and pass on his experience and knowledge gained as an investment banker and private equity professional. Josh does not only teach the basics but can readily break down and simplify complex industry concepts. Josh was not only great in teaching the technical aspects of the job but also helped to develop my strategy to succeed in interviews. Overall, I am Josh has been outstanding in helping me transition from a non-traditional background in corporate law to finance.

AY

Portfolio Manager, NorthWest Healthcare Properties REIT

Start your IB prep today.

Don’t wait to get ahead—start your IB prep today.